Zomato Q1 2025 Results: Revenue Up 2.5x, Profits Down 90% | Dekho tv news

Alright, let’s cut the corporate fluff and get real about Eternal (that’s Zomato’s parent company, just in case you spaced out for a sec) and their Q1 results for 2025. Spoiler: it’s kind of a rollercoaster.

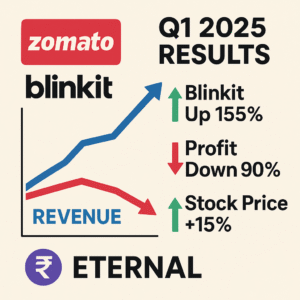

So, numbers first—because, frankly, that’s what everyone’s gawking at. The company’s net profit just faceplanted, crashing down 90% year-on-year. We’re talking ₹25 crore this quarter, compared to a whopping ₹253 crore same time last year. Ouch. They say it’s thanks to ballooning operational costs and pumping cash into Blinkit (their quick-commerce baby). Gotta spend money to make money? Maybe, but bleeding profits at this rate isn’t exactly a flex.

But hang on, revenue’s a whole different story. It shot up like a rocket—₹2,400 crore this quarter, which is nearly 2.5x what they pulled in previously. Blinkit basically went beast mode, dragging in most of that, thanks to everyone’s obsession with instant everything. Hyperpure (their B2B play) helped too, supplying restaurants and food joints who apparently can’t get enough of Eternal’s offerings.

Let’s break it down by segment real quick:

– Blinkit: The star of the show. Revenue up 155% YoY. People really, really like groceries at lightning speed, huh?

– Hyperpure: Steady growth. Not flashy, but it’s working.

– Food delivery: Still the OG moneymaker, but growth is kinda “meh” compared to the newbies. Plus, Swiggy and Zepto are breathing down their necks.

Here’s the wild bit: even with profits tanking, Eternal’s stock price went bananas, jumping almost 15% and hitting a record high. Investors either know something we don’t, or they just love a good underdog story. Or maybe everyone’s betting on quick-commerce being the next big thing.

Behind the scenes, Eternal’s basically throwing cash at new ventures, trying to own every slice of the delivery pie. The gamble? It’s expensive. Logistics, marketing, keeping up with the Joneses (read: Swiggy and Zepto)—it all adds up. And while they’re growing, the margins are getting squeezed hard. Like, stress ball hard.

Main headaches:

– Costs are blowing up. It’s not cheap to blitz a market this fast.

– Competition is fierce. Swiggy, Zepto, and a bunch of startups are gunning for the same customers.

– Profits? Yeah, investors are getting twitchy about whether Eternal can actually make this growth thing sustainable without burning through all their cash.

On the upside, there’s plenty of runway if they play it smart. Quick-commerce is hot, and Blinkit’s on fire. Hyperpure’s sneaky good too—if they double down there, it could be a sleeper hit for them. Plus, they’re betting big on tech to streamline everything, which honestly, is kinda table stakes these days.

Bottom line: Eternal’s results are a mixed bag. The topline (revenue) is killing it, but the bottom line (profits) is gasping for air. The next few quarters? Either they pull off this high-wire act, or… well, let’s just say investors might not be so chill if the profits keep nosediving. Stay tuned—this one’s far from over.

the coming quarters will be critical in determining its ability to achieve sustainable profitability and maintain its leadership position in the industry.

For Eternal, the road ahead is both challenging and promising. By addressing its cost structure, capitalizing on growth opportunities, and maintaining a customer-centric approach, the company can strengthen its position in the evolving food delivery and quick-commerce landscape.

Zomato Q1 2025 financial results breakdown | Why Zomato’s profits dropped in 2025 | Blinkit revenue growth in Q1 2025 | Eternal Zomato parent company earnings report | Quick-commerce market India 2025 analysis | Zomato vs Swiggy performance Q1 2025 | Zomato stock price jump Q1 2025 explained | How Blinkit impacted Zomato’s Q1 earnings | Zomato Q1 revenue vs profit 2025 comparison | India food delivery industry earnings 2025